The Rear View and the Front View

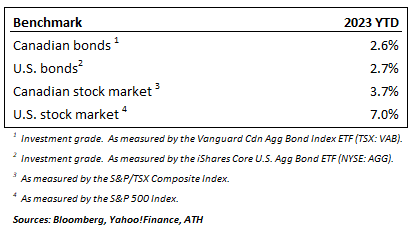

The first quarter of 2023 can be summarized in one word: VOLATILITY. Enthusiasm about China’s post-COVID re-opening, together with largely defensive investor positioning entering the new year, drove a strong January for equity markets. February brought a spate of hotter-than-expected inflation and employment data, stoking renewed fears of continued rate increases by global central banks, which drove down both bond and stock prices. March began with the emergence of a global banking crisis, which swiftly brought down bond yields. As investors became increasingly confident that the global banking crisis might be contained, they responded by driving large-cap long-duration equities higher in sympathy with now-lower bonds yields, leading to the quarterly outperformance of U.S. equity markets shown in the table below. While the S&P 500 was up 7%, the NASDAQ rose 17% and the DOW was flat, highlighting the outperformance of U.S. mega-cap technology in the quarter.

Looking ahead, the question remains…is this bull rally sustainable, or is it just a bear market rally to fade? We would lean toward the latter, for a number of reasons. To start, market breadth has been abysmal. The S&P 500’s year-to-date gain has been driven by just eight mega-cap stocks, while the other 492 stocks in the index, as a group, have fallen year to date. Some suggest it’s an investor flight to “safety”, others posit lower treasury yields are driving the YTD outperformance in mega-cap tech. Whatever the reason, it’s hard to argue a bull case when breadth is that narrow.

Furthermore, banks generally did not participate in the big recovery rally that took hold later in March. Many banks (and some insurers) remain under stress, with their equity prices slashed and their credit default swap (CDS) spreads blowing out. That sucking sound you hear is money leaving many small to medium-size regional banks toward higher-interest money market alternatives. With limited visibility on their deposit base, these banks have already began pulling back lending, tightening credit conditions.

Finally, while a recession has failed to materialize (so far) and the labor market has remained relatively strong, economic and market strength only serves to embolden the U.S. Federal Reserve to raise rates again, while the effects of their previous large rate increases continue to work their way through the system. Recent instability in the banking sector highlighted that the system is much closer to a breaking point than anyone imagined a couple months ago, but with this Fed determined to not repeat the mistakes of the 1970’s, will they raise rates again and break something badly, triggering a quick pivot to “emergency measures” mode?

In our opinion, there is a reasonable probability of that happening. If it does, we believe the Fed would de-prioritize their inflation fight in the name of financial stability. Ironically, emergency measures to ensure financial stability could just make inflation matters worse. When you consider a) the U.S. Federal Reserve has about $9 trillion on their balance sheet (built up through the past decade-plus of quantitative easing programs) b) the U.S. federal government carries $31 trillion in national debt and c) the FDIC (which insures bank deposits in the U.S.) carries $$128 billion to cover $19 trillion in bank deposits, it seems the only plausible way out of financial instability would be more “money-printing” to paper over the problems. By definition, this should be inflationary.

We’ll be carefully watching all incoming economic data, central bank speaker commentary, and of course Q1 corporate earnings reports to give us clues as this complex situation evolves.

Our Core Model Portfolios

During Q1, we took a number of portfolio actions in our core models, particularly our capital growth models. After being zero-weight in fixed income for most of 2022, we added to our bond holdings in early 2023. In particular, we added longer-duration, Canadian investment-grade exposure, with the biggest additions in the early part of Q1, as our expectation was (and still is) that we were at or near peak bond yields.

We also added to our already-overweight gold position. When the handful of U.S. regional banks faced hardship in Q1, we saw how quickly quantitative tightening gave way to yet more balance sheet expansion in the form of liquidity lines, etc. If these financial instability events persist (and we believe there is a good chance of such), we expect central banks to return to their money-printing playbooks, and with diminished confidence in crypto as a safe haven, we believe gold will be a more popular destination for investors in such a scenario.

To make room for higher fixed income and gold exposure, we reduced overall equity exposure in our capital growth models during the quarter. We also repositioned that equity exposure, for example, by adding to our Developed Asia-Pac equity allocation, as we anticipate China’s re-opening will materially benefit Australia, Japan, Korea, Singapore, and other developed Asian neighbors over the next twelve months. We maintain our underweight exposure to North American indices broadly, and we’ll continue to monitor economic and market conditions to identify opportunities to increase this allocation, if and when appropriate.