2022 Q1 Newsletter

The Rear View and the Front View

The best performing asset class in Q1 was cash, that is unless you’re the rare investor whose only holding was the Canadian equity index, which was up on the quarter. Bond and stock markets mostly fell in Q1, as the historically inverse relationship between stocks and bonds broke down yet again.

Bond markets took it on the chin in the first quarter, with the Canadian and U.S. bond markets down 7.6%1 and 6.1%2, respectively. In short, the fast move up in interest rates put relentless downward pressure on bond prices.

As for equity markets, the most interesting aspect to us was not that they were generally down on the quarter, but rather the journey they took to get there. At the time of the Russian invasion of Ukraine (Feb 24), the S&P 500 and the NASDAQ Composite had fallen year to date by 11% and 17%, respectively. The large decline in U.S. equity markets reflected a reset of investor expectations on future Federal Reserve interest rate hikes, in our opinion. The Canadian market was down just over 2% to that point, given its high weights in the outperforming energy, materials, and financial sectors. Markets remained basically flat for a couple weeks thereafter, and then staged a sharp snapback rally, though they did not fully recover their losses. The S&P 500 finished the quarter down ~5%, the NASDAQ ~9%, and S&P/TSX Composite was up ~3%.

Recall we stated in our 2021 Q3 Newsletter that our expectation was for the U.S. 10-year Treasury Note to approach 2% by the end of 2021. We were about five weeks early on that call – but we’ll take it. It took just a little longer than we expected for the U.S. Federal Reserve (and most developed-world central banks) to acknowledge that inflation is proving to be anything but transitory in the short term, and is in fact increasing and broadening. The Fed’s pivot to the inflation side of their dual mandate was rather abrupt, as they finally recognized the U.S. economy is close to maximum employment and that they’re way behind the curve on inflation. The Bank of Canada and other developed-country central banks assumed a similar posture.

The debate among investors quickly migrated from “if the Fed hikes” to “how many hikes and how quickly”. Many economists updated their forecasts to a rapid string of rate hikes over the next one to two years, culminating in a Fed funds terminal rate of 2%+. As a result, debt and equity markets reset downward to adjust to this new reality. And then…Russia invaded Ukraine.

Setting aside (but in no way diminishing) the obvious humanitarian disaster in Ukraine, from a purely economic perspective Russia’s invasion of Ukraine simply threw gasoline on the inflation fire, in our opinion. While it’s true that North American consumers are flush with cash today, and in the short term are willing to absorb higher prices from businesses across the board, the money will run out. The massive government stimulus during the pandemic is over, and 2022 will see a huge fiscal drag on the consumer. Add to that interest rates that are moving higher quickly, and top it off with significantly higher “every day” costs like food and energy and we arrive at our base case of a significant consumer-driven economic slowdown, and quite possibly a recession, beginning later 2022 or 2023.

What’s different this time is that the Fed (and other central banks) lack good options to combat this slowdown. Since the 2008-2009 financial crisis, every time there was any turbulence in the economy and/or capital markets, central banks rode to the rescue by lowering interest rates (or at least not raising them) and increasing liquidity through massive QE. Central bank actions never seemed to cause an appreciable effect on consumer inflation measures (though make no mistake…central bank behavior contributed significantly to the asset price inflation of the past decade – bonds, stocks, real estate, collectibles – you name it). This time does look different. Central banks are facing slowing economies but also high and persistent consumer price inflation. In an environment of stagflation, will they focus more on the “stag” or the “flation”? There recent commentary suggests their policy focus is on the “flation”.

Make no mistake – today’s Federal Reserve has shown itself to be nothing like the Paul Volcker Fed of the 1980’s, at least to date. The Volcker Fed did whatever was necessary to stamp out inflation, even if it hurt the economy, to ensure inflation expectations remained anchored. Post the 2008-2009 financial crisis, this Federal Reserve has repeatedly shown its dovish bias, never able to find the right time to taper QE and/or raise rates. Today they no longer seem to have a choice.

We believe the Fed and other developed-country central banks will raise rates multiple times in the coming year, as they need to be perceived as “doing something” about inflation. However, if we’re right and a significant (and potentially rapid) economic slowdown occurs, we wouldn’t be surprised if central banks pivot to the “stag” rather quickly. That is, if the economy and/or markets weaken significantly, central banks may very well pause rate hikes before they get too far down the rate-hike path, and it’s not inconceivable that they reverse course before many expect.

We suspect we are in the early stages of a bear market in equities that began at the start of this year. While the snapback rally since Feb 24 was impressive, we’re not yet convinced it was anything more than a vicious bear market rally, though we remain open to the possibility that we are still in the late stages of a bull market.

Our Core Model Portfolios

Recall from our 2021 Q4 Newsletter that our core model portfolios were defensively positioned going into 2022. Our models contained high levels cash. Our fixed income holdings were very small, and we held only short-duration, inflation-protected bonds at that. We were defensively positioned in equities. In all these respects, our defensive positioning paid off, as we were able to deploy excess cash at lower asset prices, avoid the carnage in the bond market, and generate good returns on many of our core equity holdings. That said, we further repositioned our core models in Q1 in various respects, as we discuss below.

While the Federal Reserve jawboned about inflation, they made it clear through their actions that they’re in absolutely no hurry to promote positive real interest rates. Heck, they were still buying Treasury notes and mortgage-backed securities in March as part of QE, injecting even more liquidity into the economy at a time when the exact opposite was needed. Their demonstrated lack of urgency on inflation was incredulous, and made holding any fixed income securities difficult to justify to any client concerned about their real rate of portfolio return.

We started the quarter holding only short-duration, inflation-protected bonds, as mentioned earlier. In the early part of February, we moved to the view that y/y inflation increases were peaking and so we exited these bond holdings entirely, redeploying proceeds to what we’ll deem “low risk” risk assets, specifically equities in the consumer staples and utilities sectors. These have performed very well without much downside volatility to date. Overall, our fixed income strategy over the past 12 months produced strong comparative returns relative to other fixed income assets. There will be a “right time” to re-enter bond markets, potentially at long duration and potentially soon, but we have not done so yet.

Our model portfolios hold core exposures in gold, infrastructure, and real estate. Our gold exposure performed very well in Q1, as gold started the quarter at $1,800/oz and crossed $2,000/oz before settling at around $1,954/oz at quarter-end. Similarly, our infrastructure holdings, whose revenues are largely indexed or contractually tied to inflation, performed solidly in the quarter. We continue to like our core industrial real estate holdings, despite rising interest rates, as this real estate carries relatively low debt levels and has strong secular tailwinds, in our opinion.

As for our geographic equity allocation, the outperformance of tech-heavy U.S. markets over the past ten years (and the resulting large valuation premium) motivated us to re-allocate equity exposure to other geographies early in Q1. We raised our core model weights in Canada and EMEA materially in January so that we are now underweight the U.S. relative to global equity benchmarks. EMEA, in particular, trades at a historically large discount to the U.S. market and should receive an outsized benefit from both easier monetary policy as well as a post-COVID recovery that has lagged the U.S. We also introduced a very small allocation to Emerging Markets in the quarter.

Since we implemented our new geographic weightings, our Canadian equity exposure has outperformed the broader global benchmarks, given this resource-heavy stock market has benefitted from commodity price inflation. Europe has underperformed largely due to the Russia-Ukraine conflict, and in fact we added more to our position in early March at prices distressed by the conflict. Our very small EM position has underperformed due to USD strength and negative sentiment around China de-listings from U.S. markets. That said, we remain steadfast that these changes to our core model portfolios will be the right call over the longer term.

History often rhymes

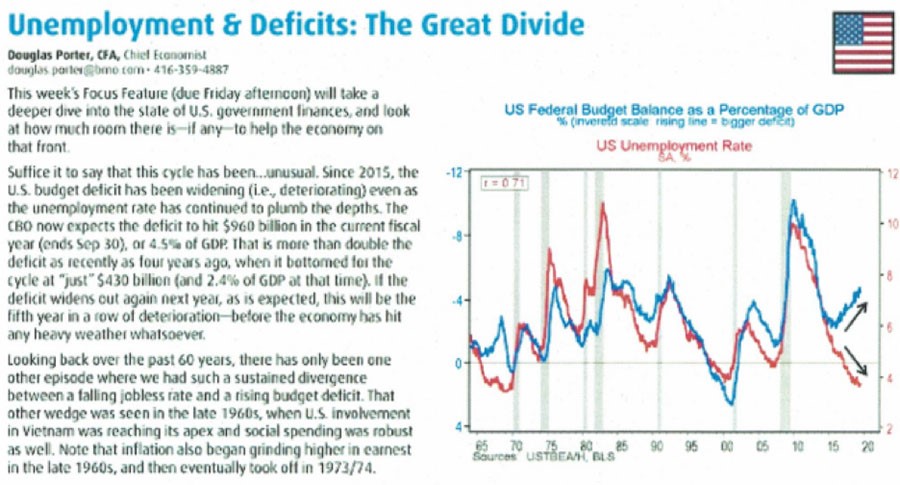

History may not repeat itself, but sometimes it sure does rhyme. We give kudos to the BMO Economics Team for publishing the chart below back in 2019 (apologies for the grainy graphic but we had no other option but to scan our printout for this piece). Since it was published, we’ve had this chart hanging on our wall as a reminder of what happens when massive deficit spending by government meets an economy operating at full employment. Recall 2019 was one year after the Trump tax cut was enacted, which of course drove an even bigger hole in the already-massive U.S. budget. It didn’t even contemplate the ~$3 billion deficits the U.S. ran in each of 2020 and 2021. Some aspects of the late 1960’s/early 1970’s (massive social spending and a war in Vietnam) are eerily similar to today. We’ll find out soon enough how much today’s central bankers have learned from the past.

1 As measured by the Bloomberg Global Aggregate Canadian Float Adjusted Bond Index.

2 As measured by the Bloomberg U.S. Aggregate Bond Index.