2022 Q3 Newsletter

The Rear View and the Front View

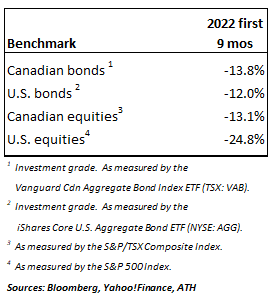

After an abysmal first half of 2022, both bonds and stock suffered further in Q3. In Q3, Canadian and U.S. investment-grade bond markets posted returns of -0.4% and -5.3%, respectively, while Canadian and U.S. stock markets posted returns of -2.2% and -5.3%, respectively. The table below presents the performance of various asset class benchmarks on a year-to-date basis:

Q3 saw some big intra-quarter gyrations, particularly in U.S. markets. For example, the S&P 500 Index found an interim bottom late in Q2, after which it moved sharply to the upside to retrace in just two months about half the ground lost since the start of 2022. However, the S&P 500 peaked on August 16 and gave back all of this ground, and more, by the end of Q3. The market essentially climbed up a mountain, and went all the way back down (and then some). U.S. investment-grade bonds were similarly (and uncharacteristically) volatile, for example the 10-year U.S. Treasury yield touched 4% in recent days after starting Q3 around 3%. We’re just not used to seeing abrupt moves like this in “risk-free” assets.

Key economic data are deteriorating, and in some cases very rapidly. We have little doubt that North American and European economies are heading toward a deeper recession later this year or early next (we say “deeper” because Q1 and Q2 actually saw successive declines in real GDP, though many have pushed the “technical” definition of recession to the wayside).

As for market valuation, we believe today’s S&P 500 forward multiple of ~16x is still too high to believe current levels represent a bottom. While 15-16x is about the long-term average for the S&P 500, we don’t think 16x is appropriate in this interest rate environment at a time where global debt is at record levels. Recall that the market bottomed during the 2008-2009 financial crisis at a P/E multiple of ~7x.

We also expect significant downward revisions to earnings in coming quarters, as companies report their second-half results and provide forward guidance in an environment of slowing demand and persistently high cost inflation.

While it’s true that the market bottoms well before the economy bottoms, it is still too early to shout the all clear, in our opinion. As Michael Hartnett (BofA Securities chief investment strategist) put it succinctly this past July, “don’t think Wall Street unwinds financial excesses of the past 13 years with a 6-month garden variety bear market”. Indeed, the central bank “punch bowl” was left on the party table far too long, spiked frequently by fiscal stimulus, and the hangover unfortunately might now also last quite a while.

Our Core Model Portfolios

Our core holdings in infrastructure, real estate, and gold remained largely unchanged in the quarter. We raised our equity exposure in the quarter by 100-200bp (depending on the model portfolio) and we continue to favour North American markets but maintain small exposure to EM equities.

Our cash levels remain high, both for defensive purposes and for flexibility to reposition when ready. As we’ve said before, it’s not ideal to have inflation erode the value of cash and cash equivalents; however, it’s far worse to generate year-to-date losses of anywhere between 13% and 25% in bond and stock markets, on top of inflationary erosion.

One highlight for the quarter was that we added some investment-grade bond exposure to our core model portfolios in the quarter. In previous newsletters, we’ve discussed our aversion to bonds in the current rate environment and won’t repeat here, and since January 2022 we’ve had a zero weighting in bonds in our model portfolios (we had held inflation-protected bonds up to that point). We felt it was now time to establish a toehold position in investment-grade paper to take advantage of attractive yields on a risk-adjusted basis as well as the opportunity for capital appreciation in the next easing cycle. Bond markets have been utterly decimated in 2022, and we continue to analyze opportunities to add to our fixed income exposure.