2022 Q4 Newsletter

The Rear View and The Front View

Happy new year, and good riddance to 2022! Yes, the past year saw the “everything bubble” finally burst. In the decade-plus prior to 2022, the combination of ultra-low manipulated rates by central banks and massive deficit spending by governments drove bubbles in multiple asset classes – bonds, equities, real estate, private debt and equity, cryptocurrencies, and much more. When money suddenly became much more expensive, that is, when central banks implemented large and rapid interest rate increases in response to inflation, the result was pain across the board, and very few places to hide.

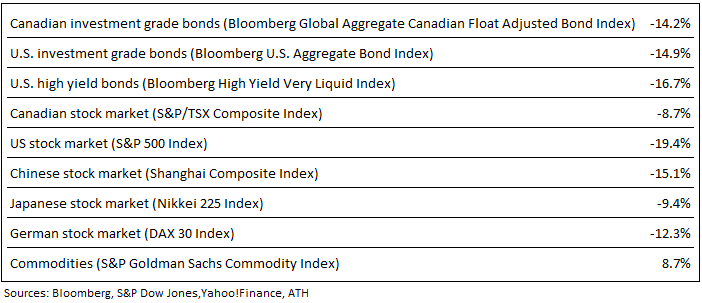

The table below, showing price returns for select capital markets in 2022, illustrates this pain:

Commodity prices, led by energy prices, were materially higher on the year, but few other markets enjoyed even a positive return in 2022. Bond markets posted generational losses, as the rise in interest rates (and commensurate fall in bond prices) was unrelenting throughout most of the year. Equity markets also saw down years, though the Canadian equity market outperformed most other developed markets, helped by its relatively high weights in energy (the best performing sector this year) and financials (down but not horribly). The broad U.S. market, as measured by the S&P 500, was down almost 20% in 2022, while the technology-heavy NASDAQ Composite – a darling in recent years – was down approximately 33% in 2022.

After a dismal performance in 2022, what will the coming year hold? In our view, an economic recession seems inevitable. There are simply too many reliable indicators pointing to a recession in 2023 – a deeply inverted yield curve, nine consecutive months of decline in the Conference Board’s Leading Economic Index, declines in manufacturing new orders for multiple months, and more. We see conditions receding quite quickly in 2023, as the lagged effects of 2022’s large and rapid rate hikes work their way through the economy. We also think inflation will come down relatively quickly as economic activity weakens, though it’s not clear to us how quickly services inflation will subside. At its last new conference of 2022, the Fed took great pains to highlight their concern about the potential stickiness of the services component of inflation, which represents ~55% of the Fed’s preferred inflation measure, the core PCE.

In regards to capital markets, we believe that 10-year note yields have likely peaked in both Canada and the U.S. That doesn’t mean we think those yields will come down quickly, as Quantitative Tightening (QT) by central banks will be a persistent overhang on bond markets. That said, we don’t see a repeat of 2022 in credit markets. As for equity markets, we know from history that markets bottom well before an economic recovery takes hold, therefore the key consideration for us is timing. Will markets find a bottom fairly quickly (as they did during the 2008-2009 GFC) or will they embark on a much longer journey down (as they did post the dot-com bust in 2001) before they finally find a bottom?

Our Core Model Portfolios

After holding 0% bond exposure in all our core model portfolios through the first 10 months of 2022, we introduced Canadian investment-grade exposure in Q4, at a weighted average duration lower than the overall market. With yields at or near peak, in our view, we felt it was finally time to initiate a position. We also increased gold exposure in our core models, as we believe central banks are nearing the end of their tightening cycles. Our expectation of further USD weakness in the first half of 2023 will also provide a tailwind for precious metals prices.

The most notable changes to our equity exposure in Q4 were a reduction in our Canadian exposure and an increase in our emerging markets exposure. We reduced our Canadian equity exposure materially in Q4 after what had been an 18-month period of outperformance by Canada over most developed-country markets. We also, and quite recently, increased our emerging markets equity exposure across all our core models, based on a historically wide valuation gap between EM and the U.S. (as measured by the S&P Cape-Shiller P/E ratio) and our expectation of further USD weakness. Just as we’ve been throughout 2022, we remain underweight the U.S. equity market vs. the ACWI as we start 2023.